The Spread Isn’t Alpha

What credit default swaps reveal about $100 million in Illinois public money, and the question nobody is asking about state investment policy.

On January 6, 2026, Palm Beach County Comptroller Mike Caruso announced that the county had purchased another $350 million in Israel Bonds. The new buy brought the county’s position to exactly one billion dollars, making Palm Beach the largest local-government holder of Israel Bonds in the world. Caruso, a CPA by training, was careful with his framing. “Investment policy is not politics,” he said. “It is purely a function of safety, liquidity, and market rate of return. Israel Bonds are paying a higher rate than other allowable investment alternatives, including U.S. Treasuries.”

Three months earlier, the North Carolina Treasurer’s office had done the opposite. After several years of letting the position run off without any new purchases, the office quietly sold its remaining $6.7 million in pension holdings. The Treasurer’s office told a coalition of activists pushing for divestment that the state hadn’t been adding to the position for a simple reason: they weren’t finding it compelling from a risk-and-return perspective.

Two state-level fiduciaries, both bound by statutory investment criteria, reached opposite conclusions about what the math says.

The question that organizes itself is which one is right.

The answer turns out to be more useful than either side of the public debate has acknowledged. There is a market-implied tool that almost nobody in this conversation has been using, and when you apply it, both of the standard arguments collapse in different directions. A sharper question emerges from the wreckage.

This piece is an attempt to lay out what that tool shows.

The frame that isn’t working

The public debate about state investment in Israel Bonds has been running on two parallel tracks for two and a half years.

The first track is moral. Israel Bonds are general-obligation debt: the State of Israel uses the proceeds for any purpose, including military spending. For people who object to Israeli government policy on civil-rights or international-humanitarian grounds, that fungibility is the issue. The frame is conscience and complicity.

The second track is financial. State treasurers point to coupons, default histories, and spreads over U.S. Treasuries. Israel has never missed a payment on Israel Bonds in seventy-plus years. The yield premium has typically run between 100 and 150 basis points over comparable Treasuries. For a fiduciary operating under a statutory obligation to seek market return, that looks like a defensible investment.

These two arguments do not engage each other. They run on different vocabularies, in different rooms, with different evidentiary standards. The moral argument operates on conscience. The financial argument operates on yield. Neither side concedes anything to the other, and neither side needs to, because they are not actually debating the same thing.

What is missing from both is the market’s own answer to the question. That answer is now available.

What CDS prices say

A credit default swap is an insurance contract on sovereign debt. The buyer pays a periodic premium; the seller agrees to compensate the buyer if the sovereign defaults. The premium, called the CDS spread, represents the market’s collective real-time estimate of how likely default is. It strips out duration, currency, coupon convention, and everything else that complicates a comparison of bond yields. It just prices the probability of getting wiped out.

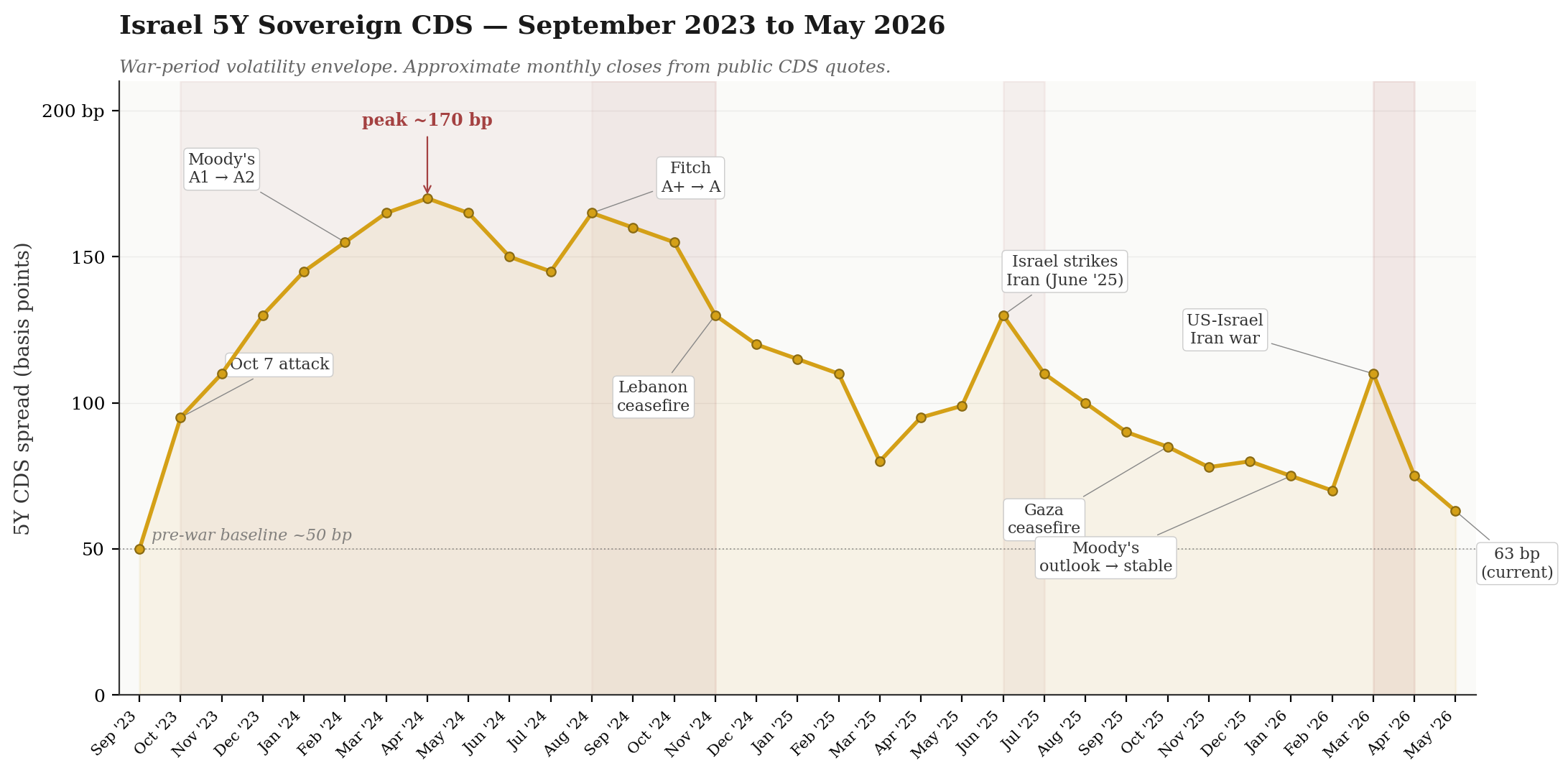

Israel’s five-year CDS spread, as of mid-May 2026, sits at 63 basis points. That is the market’s price today, on the risk that the State of Israel defaults on its dollar debt within the next five years.

The arc is what you would expect from a sovereign that fought a multi-front war and then settled. The pre-war baseline was about 50 bp. The Hamas attacks on October 7, 2023, pushed the spread into a sustained climb. Moody’s first downgrade took it past 150 bp by February 2024. The peak, roughly 170 bp, came in April 2024, around the Iranian direct strike on Israel. The Fitch downgrade in August 2024 kept things elevated. The Lebanon ceasefire in late 2024 marked the beginning of the compression. Israel’s June 2025 strikes on Iran produced a transient spike. The 12-day U.S.-Israel war against Iran in February-April 2026 produced another spike to around 110 bp, which has now fully unwound. Israel CDS is currently at the low of the entire post-war range.

Markets have priced through the geopolitical risk premium of the past two and a half years. The implied probability that Israel defaults in the next five years, using the standard 40-percent recovery rate assumption, is about 5 percent cumulative, roughly 1 percent per year. That is not a fragile credit.

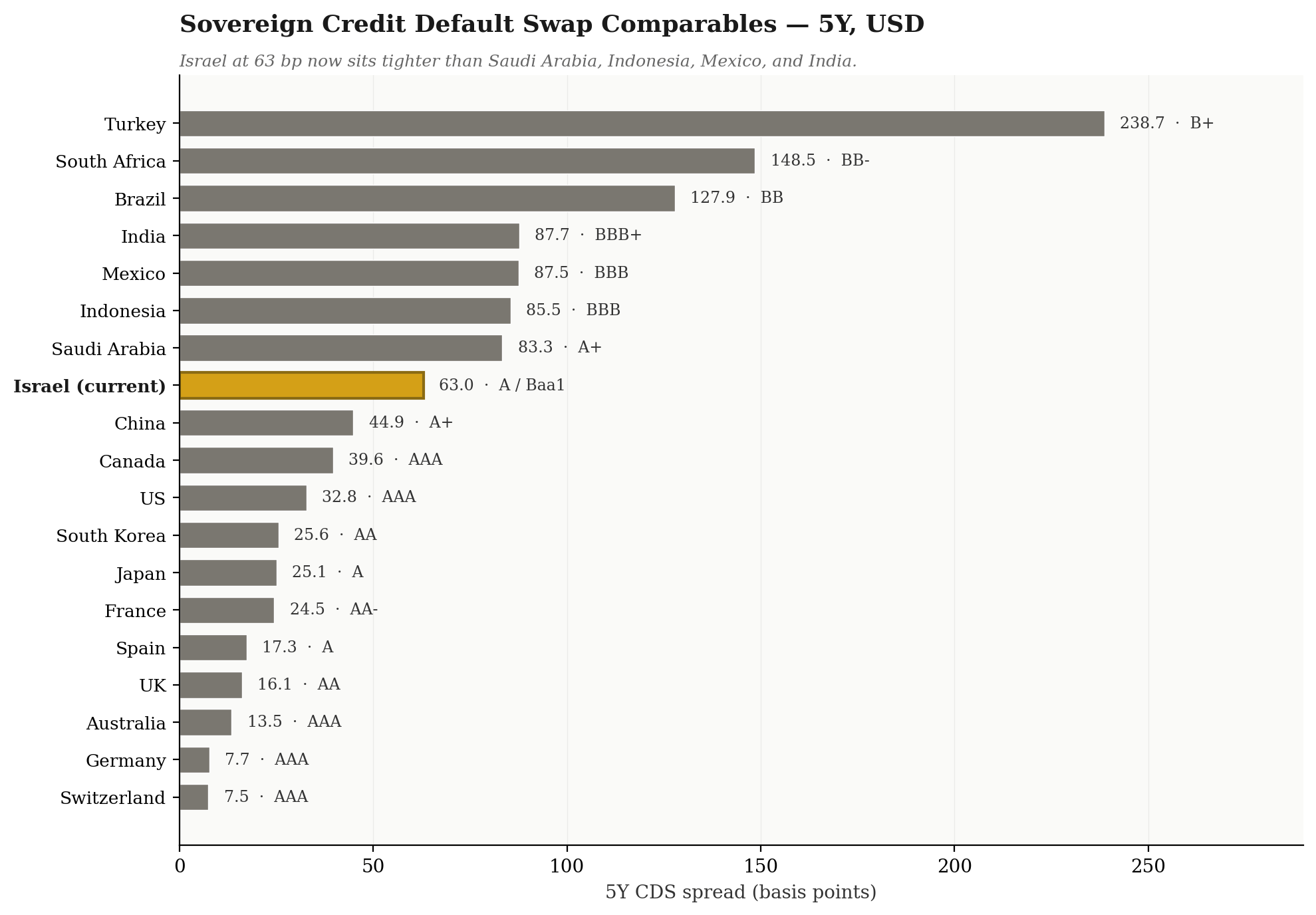

It is also, more interestingly, a credit being priced more tightly than its formal ratings would suggest.

Israel’s 63 bp CDS sits below Saudi Arabia at 83 bp, Indonesia at 86 bp, Mexico at 88 bp, and India at 88 bp. Each of those countries carries a comparable or formally lower credit rating. The market is pricing Israel as cleaner credit than the rating agencies, by a measurable margin.

This is the first thing that breaks. The argument that Israel Bonds is somehow a financially imprudent investment, the argument that various divestment campaigns have made, and the argument that the North Carolina Treasurer’s office gestured at do not withstand contact with CDS data. The market does not think Israel is a stressed credit. It thinks Israel is a roughly A-tier sovereign, currently priced more like A+ than like Moody’s Baa1.

So one side of the financial debate is wrong on the data.

The other side is wrong too, and for a reason that turns out to matter more.

What 114 basis points actually pays for

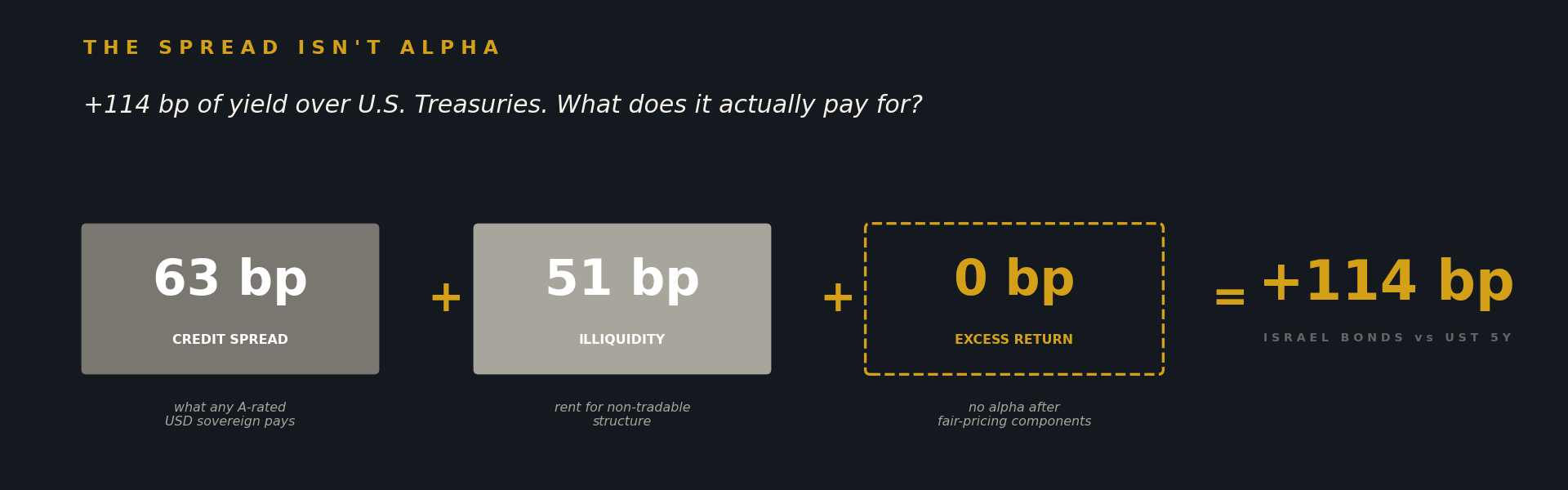

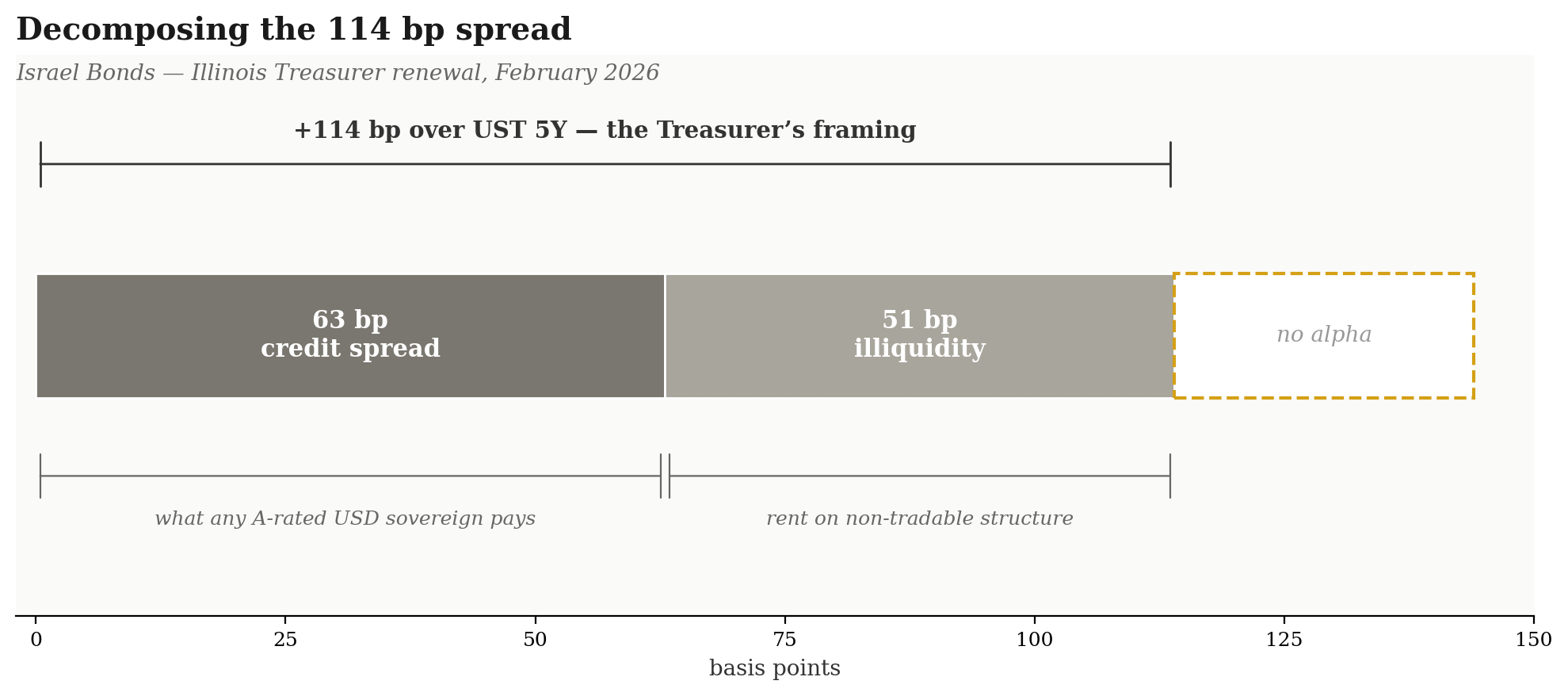

When Illinois Treasurer Michael Frerichs renewed $15 million in Israel Bonds this past February, his office announced it the way every state treasurer announces these purchases. The bond paid 4.86 percent on a five-year maturity. That outperformed a comparable U.S. Treasury by about 114 basis points, which the Treasurer’s office characterized as 23 percent additional return for Illinois taxpayers.

114 basis points sounds like a lot. It is, in the absolute. But that framing imports an assumption that does not survive examination: that Treasuries are the right benchmark.

A Treasury is risk-free. Israel Bonds are not. They carry sovereign credit risk and an additional structural feature that ordinary sovereign bonds lack: they are non-tradable. There is no secondary market, no way to sell into a crisis, no daily mark-to-market price. You hold to maturity, or you do not hold.

The 114 basis points are not the free yield. It is compensation for taking on credit risk and giving up liquidity. CDS data lets you see exactly how much for each.

Sixty-three basis points is the credit spread, the compensation any A-rated USD sovereign bond would pay for the credit risk involved. It is the standard market price for accepting that this is not a Treasury. Fifty-one basis points is the illiquidity premium, the compensation for accepting the non-tradable structure, derived by comparing the Israel Bonds yield to Israel’s actively traded USD eurobonds of similar maturity.

What remains after stripping out those two is the excess return, the alpha, that an investor earns relative to a fair-priced equivalent.

That number, on the math, is approximately zero. Possibly slightly negative, since Israel CDS now prices tighter than peers like Saudi Arabia, meaning a fair-priced equivalent would actually pay slightly less than 114 bp over Treasuries.

Israel Bonds are not a bad investment. They are not a good investment. They are a fairly priced investment. Holding them is neither financially imprudent nor financially generous. The instrument clears the market the same way any A-rated sovereign instrument with restricted liquidity does.

Once that lands, the entire framing of the debate falls apart.

What is actually being decided

The Treasurer’s defense rests on the premise that the position generates value for taxpayers. The decomposition shows that the position generates the standard market price for the risks it carries. No surplus. No discount. Market clearing.

The divestment activist’s critique rests on the premise that the security is somehow financially problematic, the kind of thing prudent fiduciaries should avoid on its risk profile alone. The decomposition shows that the security pays exactly what it should pay.

Both sides have been arguing about whether Illinois should hold an investment that delivers an excess return. The market says no such investment exists. The 114 bp spread is rent on credit and rent on illiquidity, both fairly priced. There is no surplus to defend or to criticize.

What is left, once both financial pretenses come down, is a question that nobody on either side has been asking with any clarity. If the financial case is neutral, why is this particular security being chosen by these particular officials over the dozens of other foreign sovereign instruments that meet the same statutory eligibility tests? That is not a financial question. It is a question about the decision-making process. It is, in other words, a fiduciary-procedure question. And the procedural question is the part of this whole conversation that turns out to have actual structural leverage.

The Illinois architecture

Most public discussion of “Illinois’s investment in Israel Bonds” treats Illinois public money as a single pot. It is not. Several distinct fiduciary regimes operate in parallel, with different oversight, different disclosure rules, and different statutory authority.

The two that matter most for this conversation:

The Illinois State Treasurer’s Office manages approximately $39 billion in state operating funds, including cash from tax receipts, fees, and fund balances awaiting disbursement. Treasurer Michael Frerichs is the sole fiduciary. Decisions are his alone, within statutory eligibility criteria. The $100 million Israel Bonds position lives here. Every purchase comes with a public press release naming the amount, coupon, and maturity. That visibility is why everyone knows about it.

The Illinois State Board of Investment, ISBI, is a nine-member board with fiduciary responsibility for the pension assets of three of the state’s pension systems: the State Employees Retirement System (about $24 billion), the Judges’ Retirement System (under $1 billion), and the General Assembly Retirement System (under $100 million). Frerichs serves on the board as Vice Chair. ISBI does not publish line-item holdings. Whatever Israel's exposure pension money has at this level is not externally verifiable from public filings.

These are different pots. They get routinely conflated in public conversation, and that conflation has been expensive for everyone trying to think clearly. When divestment campaigns target “Illinois’s investment in Israel Bonds,” they almost always mean the Treasurer’s $100 million, because that is the only piece publicly disclosed. The pension systems operate under entirely different rules.

And ISBI is only three of Illinois’s pension systems. The Teachers’ Retirement System (TRS, about $79 billion, 456,000 members) has its own independent fifteen-member board. The Illinois Municipal Retirement Fund (IMRF, about $55 billion, 520,000 members, and the only Illinois pension system that is actually well-funded at 95.8 percent) has its own elected eight-member board. The State Universities Retirement System (SURS, with about $25 billion in assets) has its own eleven-member board. The Chicago Teachers’ Pension Fund (CTPF, with about $13.7 billion in assets) is separate from all of them. Plus the Chicago municipal pension funds, the Cook County funds, the police and fire funds, and the roughly 660 downstate police and fire pension funds.

“The Illinois pension system” is a sentence with at least five major subjects and dozens of minor ones. Effective intervention has to specify which one.

The statutory lever

The Treasurer’s $100 million sits within a statutory eligibility framework that imposes two binding tests on foreign sovereign investments. To be eligible, a foreign sovereign issuer must have met its bond payment obligations for at least 25 consecutive years and must be rated in the three highest classifications by at least two nationally recognized rating services.

Israel passes the first test. The Israel Bonds program has honored payments since 1951. Israel currently passes the second test on the strength of S&P’s A rating and Fitch’s A rating. Both of those agencies still classify Israel in their top three categories: AAA, AA, A.

Moody’s, which downgraded Israel from A1 to Baa1 in two separate moves across 2024, including an unusual two-notch jump from A2 to Baa1 last September, has Israel in its fourth category. Under one common reading of the “three highest classifications” language, Moody’s may not already count toward the statutory eligibility test. Which means Israel’s current statutory eligibility hangs on S&P and Fitch both staying at A or above.

A single-notch downgrade by either of those agencies to BBB+ or below would mean Israel has only one rating service classifying it in the top three categories. The statute would no longer be satisfied. The Treasurer would have no authority to continue holding the position, regardless of his preferences, and the bonds would automatically become ineligible at the next purchase decision.

This is the most consequential fact in the entire conversation, and almost nobody is talking about it.

Both S&P and Fitch have restored their outlooks to stable as of late 2025 and early 2026, following the ceasefires. But the rating-action cycle is reactive to events on the ground, not to outcomes anyone has guaranteed. A renewed conflict, a fiscal deterioration, or a debt-service stress event could prompt another notch move at either agency. If it happens at the wrong agency, the question of whether Illinois holds Israel Bonds gets answered by statute, not by anyone’s political preference.

For anyone trying to think about leverage in this conversation, that is the lever. It is automatic. It does not require legislative action. It does not require political will. It only requires that the rating agencies do what rating agencies do, and the relevant agencies are S&P and Fitch.

Illinois in the national context

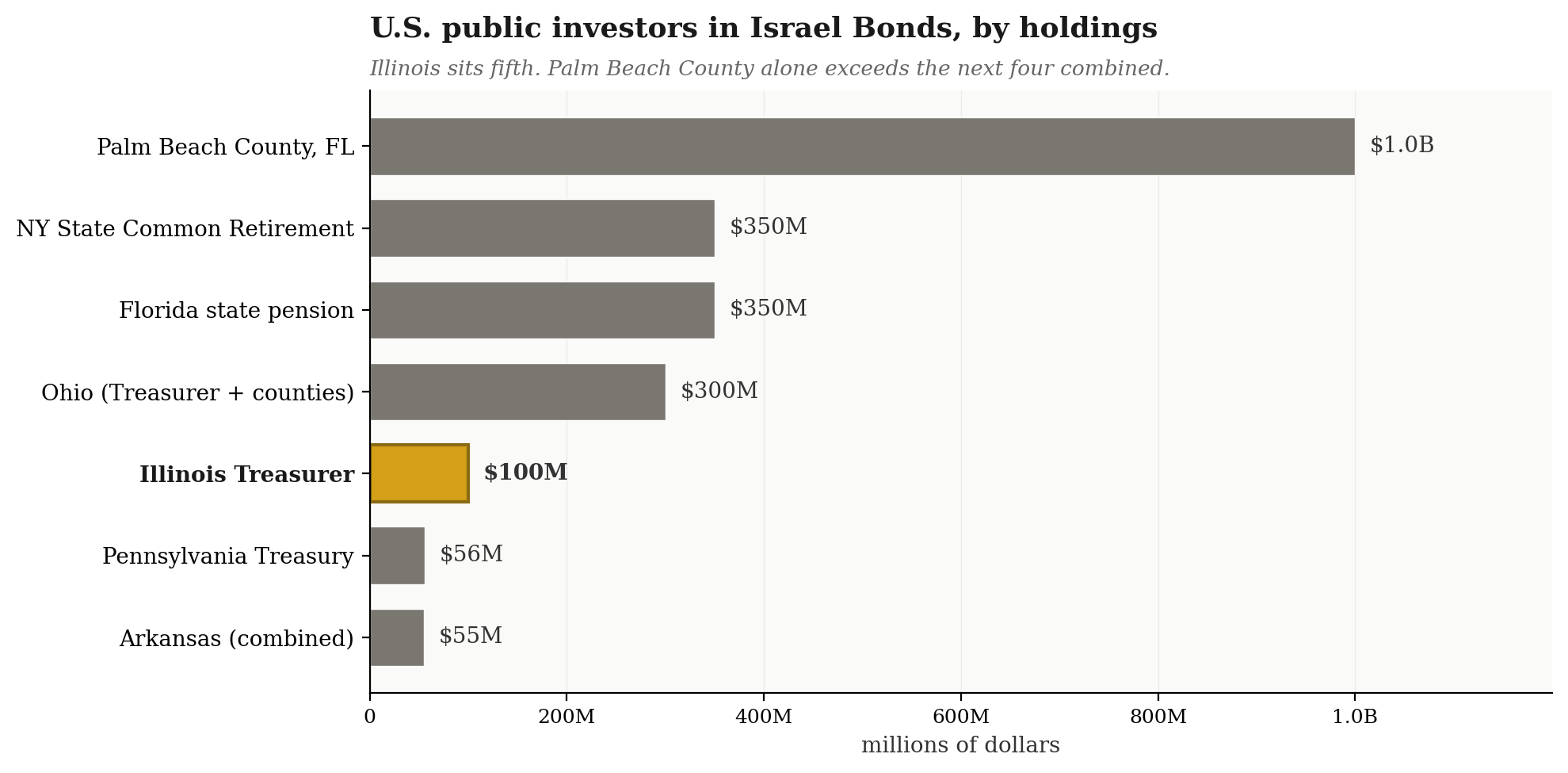

Illinois is one node in a national pattern. Since October 2023, U.S. state and local treasuries have purchased over $1.7 billion in Israel Bonds across more than 35 jurisdictions.

Illinois sits fifth. Palm Beach County alone exceeds the next four combined. The Illinois $100 million is a meaningful position by Treasury standards (about 0.25 percent of the state operating portfolio), but it is small relative to the leading state holders and dwarfed by Palm Beach.

Movement in the other direction is starting too, though the dollar amounts are modest. North Carolina sold its pension position late in 2025. New York City, under former Comptroller Brad Lander, stopped new purchases for the city pension. Active divestment campaigns are tracked by Jewish Voice for Peace and Palestinian-led partner organizations across more than 10 states, with ongoing efforts in New York State, Ohio, Pennsylvania, and Miami-Dade County.

The North Carolina pattern is the most legally durable of these. The Treasurer’s office did not cite human rights. It did not invoke international law. It did not engage the moral argument. What it told the divestment coalition, by accounts from people in those conversations, was that the office no longer found the position compelling on risk-and-return grounds. That is a fiduciary-frame argument, made within the standard investment-policy review process, requiring no legislation. It does not trigger anti-BDS preemption statutes because it is not a boycott motivated by national-origin animus. The fiduciary review concludes that the security is not compelling.

This is, in my reading, the most analytically defensible path forward for state-level officials who want to move away from these holdings. It does not require winning the moral argument. It does not require winning a legislative fight. It requires asking treasurers and pension boards a procedural question they are already required under existing law to answer. What review process governs the choice to hold this security over other eligible alternatives? How is that process documented? What disclosure accompanies the decision?

For state-level Treasurer holdings, that question lands on a single elected official, in a context where the press-release norm has already established a high disclosure baseline. For pension-system holdings, it lands on boards with explicit fiduciary obligations under the state pension code. Either way, the question is procedural rather than substantive. It does not ask the official to take a position on a contested international conflict. It asks them to document and defend their decision-making process, which, under existing law, they are already required to do.

The choice that requires articulation

What CDS data has done is establish, with as much market authority as anything ever gets established, that the financial premise underlying the standard defense of these holdings is not what it appears to be. The 114 basis points over Treasuries is not alpha. It is rent on credit and illiquidity, paid by the State of Israel and collected by the holder, in roughly the amount that any other A-rated sovereign would pay. That is not a critique. It is just what the market shows.

The choice to hold this security, when fair-priced alternatives exist, requires articulation. Not as a confession. As a normal incident of fiduciary review. The Treasurer cannot honestly say this is a high-return investment. The activist cannot honestly say this is a financially imprudent investment. Both have been wrong, in opposite directions, on the same data. What replaces both is a more concrete question about the decision-making process, situated within a body of public investment law that is much better suited to the question than either the moral framework or the financial-prudence framework that has been doing the work so far.

Illinois has $100 million on the table, statutorily authorized, fairly priced, and held in a portfolio whose decision-maker is required by Illinois statute to make those decisions on fiduciary criteria. The question worth asking, in that exact frame, is what the fiduciary criteria are, how the choice among eligible foreign sovereigns is documented, and what disclosure accompanies the decision. That is a question that existing law already requires an answer to.

The most useful thing the CDS analysis does is tell us that, whatever the answer turns out to be, it cannot be “because this is the best return available.” The math does not support that claim. The market does not support that claim. The answer will need to be something else.

Articulating that something else, on the public record and with documentation that survives fiduciary review, is the move actually available here? It does not require winning the argument that nobody has been winning for the past two and a half years. It only requires that officials do, on the public record, what their fiduciary obligations already require them to be doing on the public record.

That is what the spread, properly decomposed, makes possible.

Sources: investing.com daily CDS quotes; Moody’s, S&P, and Fitch rating actions; Illinois Treasurer’s office press releases; relevant pension fund annual reports; Bond Buyer; Times of Israel; Palm Beach County Clerk’s office press releases. CDS trajectory chart shows approximate monthly closes; precise daily values vary intra-month.

Written in a personal capacity. Views are my own and do not represent GrayStak or any other affiliated organization. The author holds no financial positions in Israel Bonds, has no compensated relationship with the Illinois Treasurer’s Office, the Development Corporation for Israel, or any divestment coalition, and has not been paid to write this piece. CDS values are approximated from public sources; precise daily quotes vary. Statutory interpretations reflect the author’s reading and have not been adjudicated in court. The account of the North Carolina Treasurer’s Office’s reasoning is reconstructed from public reporting and descriptions of those conversations by divestment coalitions; the office has not made formal public statements directly addressing Israel Bonds as a category. I have written in other contexts on regional foreign policy and political risk questions; this piece is procedural and analytical rather than positional. Not investment advice.